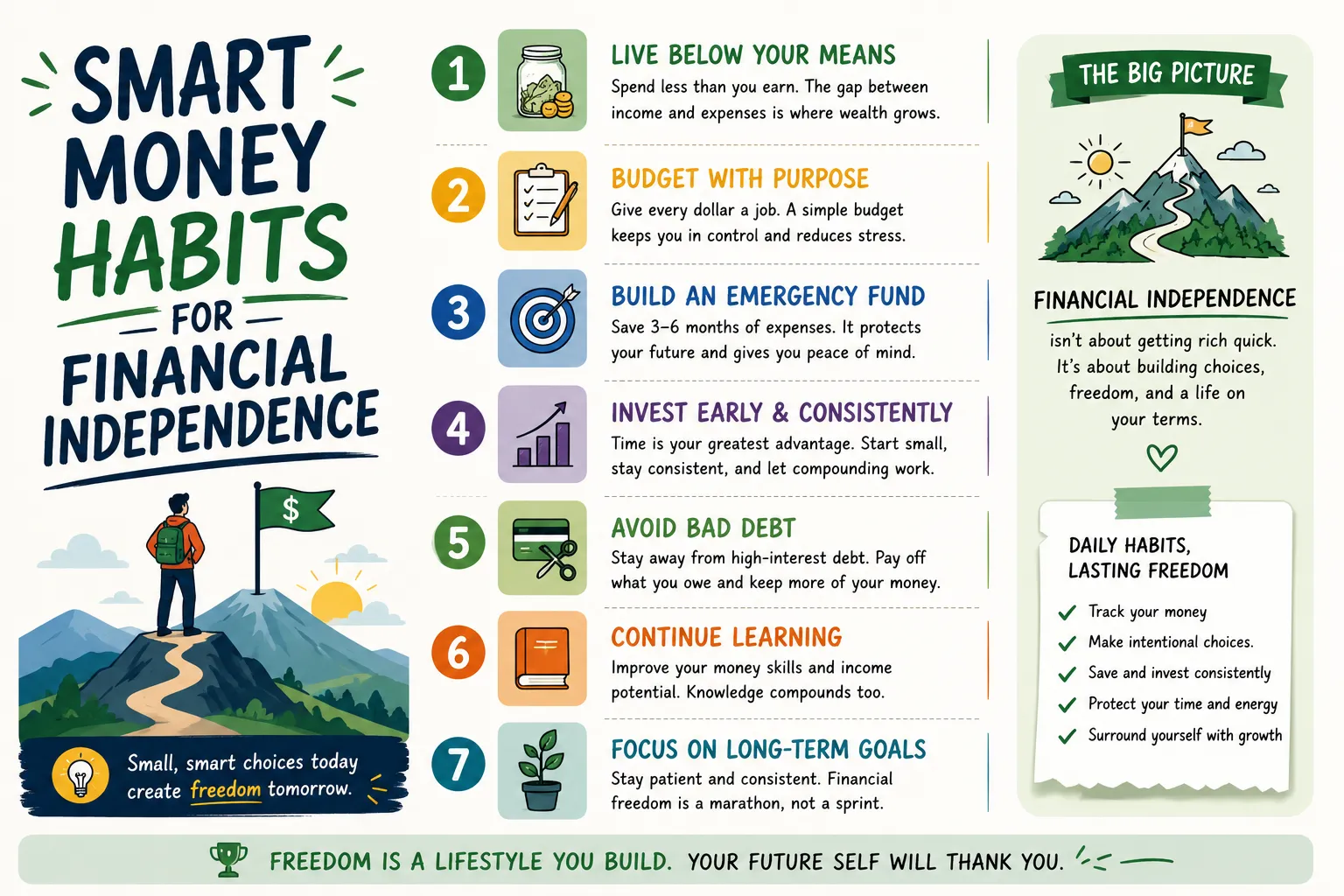

Smart Money Habits for Financial Independence

Financial independence is no longer a dream reserved for high-income earners, entrepreneurs, or investment professionals. In today’s economy, individuals who consistently practice smart money habits can create lasting wealth, enjoy financial security, and achieve the freedom to make life decisions without being controlled by financial stress. Whether your goal is early retirement, passive income generation, wealth accumulation, or simply living comfortably without debt, developing effective money habits is the foundation of long-term success.

The journey toward financial independence is not built on luck. It is built through disciplined financial behavior, strategic investing, intelligent budgeting, tax-efficient planning, and continuous wealth optimization. Many people focus on earning more money, but true financial independence comes from managing, growing, and protecting your money effectively.

In this comprehensive guide, we will explore the most impactful money habits that can help you create sustainable wealth, improve your financial future, and establish long-term financial freedom.

What Is Financial Independence?

Financial independence means having enough assets, investments, and passive income sources to cover your living expenses without relying entirely on active employment. It provides flexibility, security, and the ability to make choices based on personal goals rather than financial necessity.

Financially independent individuals often focus on:

- Building diversified investment portfolios

- Creating multiple income streams

- Minimizing unnecessary debt

- Practicing intentional spending

- Maximizing savings rates

- Utilizing tax-efficient investment strategies

- Protecting assets through proper risk management

Habit #1: Pay Yourself First

One of the most powerful financial habits is paying yourself first. Before paying bills, shopping, or discretionary expenses, allocate a percentage of your income directly toward savings and investments.

Many successful investors automate contributions to:

- Retirement accounts

- Index funds

- Dividend portfolios

- High-yield savings accounts

- Emergency funds

- Brokerage investment accounts

This strategy ensures wealth building becomes automatic rather than dependent on monthly discipline.

Habit #2: Create a High-Performance Budget

A budget is not about restriction—it is about optimization. High-net-worth individuals often monitor cash flow carefully because every dollar has a purpose.

An effective budget should include:

| Category | Recommended Allocation |

|---|---|

| Housing | 25% - 35% |

| Savings & Investments | 20% - 40% |

| Transportation | 10% - 15% |

| Insurance | 5% - 10% |

| Food | 10% - 15% |

| Entertainment | 5% - 10% |

Tracking expenses regularly allows you to identify spending leaks and redirect money toward wealth-building opportunities.

Habit #3: Build a Fully Funded Emergency Reserve

Unexpected events can derail even the best financial plans. Job loss, medical emergencies, economic downturns, and unexpected repairs can create financial hardship.

A properly funded emergency reserve should ideally cover:

- 3-12 months of living expenses

- Mortgage or rent payments

- Utilities and insurance costs

- Healthcare expenses

- Essential household costs

Keeping emergency funds in highly liquid accounts helps protect investments from being sold during unfavorable market conditions.

Habit #4: Eliminate High-Interest Debt

High-interest debt significantly slows wealth creation. Credit card balances, personal loans, and other high-interest obligations often generate guaranteed negative returns.

Debt reduction strategies include:

- Debt avalanche method

- Debt snowball method

- Debt consolidation

- Balance transfer optimization

- Interest rate negotiation

Eliminating high-interest liabilities effectively increases your available capital for investing and long-term wealth accumulation.

Habit #5: Invest Consistently Regardless of Market Conditions

Many investors attempt to time markets. Successful wealth builders focus instead on consistent investing.

Dollar-cost averaging allows investors to:

- Reduce emotional investing decisions

- Take advantage of market volatility

- Build positions steadily over time

- Benefit from long-term market growth

Consistency often outperforms attempts to predict short-term market movements.

Habit #6: Understand the Power of Compound Growth

Compound growth is one of the strongest forces in wealth creation. The earlier you begin investing, the greater the impact of compounding returns.

| Monthly Investment | Years | Estimated Value at 8% |

|---|---|---|

| $250 | 20 | $147,000+ |

| $500 | 20 | $294,000+ |

| $1,000 | 20 | $589,000+ |

| $2,000 | 20 | $1.17 Million+ |

The combination of time, discipline, and reinvestment can produce extraordinary long-term results.

Habit #7: Diversify Investment Holdings

Diversification helps reduce risk while maintaining growth potential. Financially independent investors typically avoid concentrating all assets into a single investment.

A diversified portfolio may include:

- Domestic equities

- International stocks

- Real estate investments

- Index funds

- Dividend-paying companies

- Government bonds

- Corporate bonds

- Alternative investments

Diversification improves portfolio resilience during market fluctuations.

Habit #8: Increase Income Through Skill Development

Investing in yourself often generates some of the highest returns available. High-income skills can significantly accelerate wealth creation.

Examples include:

- Digital marketing

- Software development

- Artificial intelligence expertise

- Data analytics

- Sales leadership

- Project management

- Financial consulting

- Business strategy

Continuous learning expands earning potential while creating greater investment capacity.

Habit #9: Develop Multiple Streams of Income

Relying solely on a paycheck creates financial vulnerability. Wealthy individuals often establish multiple income sources.

Potential income streams include:

- Dividend income

- Rental property income

- Online businesses

- Consulting services

- Digital products

- Affiliate marketing

- Royalty income

- Investment distributions

Multiple revenue sources improve financial stability and accelerate wealth accumulation.

Habit #10: Optimize Tax Efficiency

Tax planning plays a major role in wealth preservation. Many investors focus heavily on returns while overlooking tax optimization opportunities.

Effective tax strategies may include:

- Tax-advantaged retirement accounts

- Capital gains planning

- Tax-loss harvesting

- Business expense optimization

- Asset location strategies

- Charitable contribution planning

Reducing tax liabilities legally can significantly improve long-term investment growth.

Habit #11: Protect Wealth Through Insurance Planning

Building wealth is only part of the equation. Protecting accumulated assets is equally important.

Financial protection strategies include:

- Health insurance

- Life insurance

- Disability coverage

- Property insurance

- Liability protection

- Umbrella insurance policies

Proper risk management prevents unexpected events from causing major financial setbacks.

Habit #12: Review Financial Goals Regularly

Financial independence requires ongoing evaluation. Reviewing goals quarterly or annually helps maintain focus and accountability.

Key areas to evaluate include:

- Net worth growth

- Investment performance

- Savings rate

- Debt reduction progress

- Income growth

- Retirement projections

Tracking measurable progress helps identify opportunities for improvement.

Habit #13: Avoid Lifestyle Inflation

One of the most common obstacles to wealth creation is lifestyle inflation. As income increases, spending often rises proportionally.

Financially successful individuals frequently maintain moderate lifestyles even as earnings grow. This creates a larger gap between income and expenses, allowing more capital to be invested for future growth.

Instead of upgrading every aspect of life with each raise, prioritize increasing investments and wealth-producing assets.

Habit #14: Focus on Long-Term Thinking

Financial independence is rarely achieved through short-term speculation. Long-term investors understand that markets fluctuate, economies evolve, and wealth takes time to build.

Long-term thinking encourages:

- Patience during volatility

- Consistent investing behavior

- Reduced emotional decision-making

- Greater portfolio growth potential

Time is often the most valuable asset available to investors.

Habit #15: Prioritize Financial Education

The financial landscape continues to evolve rapidly. Individuals who remain informed are better positioned to identify opportunities and avoid costly mistakes.

Areas worth studying include:

- Personal finance

- Investment management

- Economic trends

- Tax planning

- Real estate investing

- Retirement planning

- Business ownership

- Asset protection

Financial literacy compounds just like investment returns.

Common Mistakes That Delay Financial Independence

| Mistake | Impact |

|---|---|

| Overspending | Reduces savings potential |

| Not Investing Early | Loses compounding advantages |

| High-Interest Debt | Consumes future wealth |

| Lack of Diversification | Increases portfolio risk |

| No Emergency Fund | Creates financial instability |

| Poor Tax Planning | Reduces net returns |

| Emotional Investing | Leads to costly mistakes |

Building Your Personal Financial Independence Roadmap

A successful roadmap typically follows several phases:

- Establish financial awareness.

- Create and optimize a budget.

- Build emergency reserves.

- Eliminate expensive debt.

- Increase savings rates.

- Invest consistently.

- Create multiple income streams.

- Optimize taxes and risk management.

- Expand investment diversification.

- Reach financial independence milestones.

Each phase builds upon the previous one, creating a strong foundation for sustainable wealth growth.

Final Thoughts

Financial independence is not achieved through a single investment, market prediction, or financial shortcut. It is the result of disciplined habits practiced consistently over many years. Smart budgeting, strategic investing, tax optimization, debt management, income diversification, and continuous financial education work together to create lasting wealth.

The most successful wealth builders understand that financial freedom is a process rather than an event. Every dollar saved, invested, and protected contributes to a stronger financial future. By adopting these smart money habits and remaining committed to long-term goals, you can create financial security, expand opportunities, and ultimately achieve true financial independence.