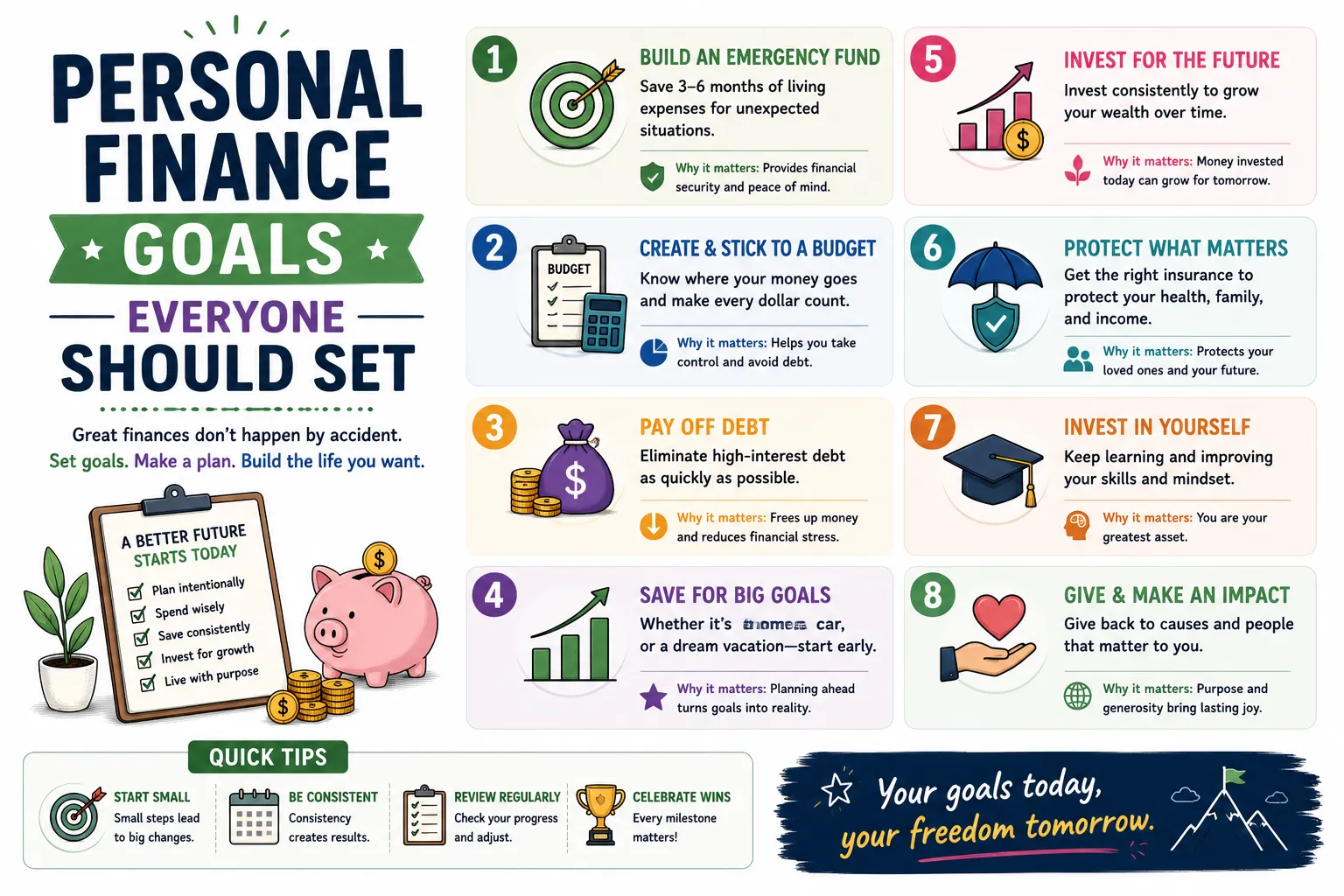

Personal Finance Goals Everyone Should Set

Personal finance success does not happen by accident—it is the result of clear planning, disciplined execution, and consistent progress toward well-defined financial goals. Whether someone is just starting their career or already managing a stable income, setting structured financial goals is essential for building wealth, reducing financial stress, and achieving long-term independence.

Without clear goals, money often gets spent without direction. But when financial objectives are defined, every rupee or dollar earned can be assigned a purpose—saving, investing, debt reduction, or lifestyle improvement. This intentional approach transforms financial behavior and accelerates wealth creation.

This comprehensive guide explores the most important personal finance goals everyone should set, regardless of income level, profession, or age group.

Why Setting Financial Goals Matters

Financial goals act as a roadmap for money management. They provide clarity, motivation, and structure for financial decisions.

Key benefits include:

- Better control over spending habits

- Improved savings discipline

- Faster debt reduction

- Clear investment direction

- Reduced financial stress

- Long-term wealth accumulation

Without goals, financial progress becomes inconsistent and unpredictable.

Short-Term Financial Goals (0–2 Years)

Short-term goals focus on immediate financial stability and building strong foundations for future wealth creation.

1. Build an Emergency Fund

An emergency fund is one of the most important financial safety nets. It protects against unexpected expenses such as job loss, medical emergencies, or urgent repairs.

| Emergency Fund Level | Coverage |

|---|---|

| Basic | 3 months of expenses |

| Recommended | 6 months of expenses |

| Strong Security | 12 months of expenses |

A strong emergency fund ensures financial stability during uncertain times.

2. Create a Monthly Budget

A budget helps track income and expenses effectively.

A common structure is:

- 50% needs

- 30% wants

- 20% savings and investments

Budgeting provides visibility and control over financial decisions.

3. Eliminate High-Interest Debt

Debt such as credit card balances can significantly reduce financial progress due to high interest rates.

Debt reduction strategies include:

- Debt avalanche method

- Debt snowball method

- Balance consolidation

- Refinancing options

Reducing debt improves cash flow and financial flexibility.

Medium-Term Financial Goals (2–7 Years)

Medium-term goals focus on building wealth and improving financial stability.

4. Save for Major Life Purchases

Major expenses require structured saving plans to avoid unnecessary debt.

Examples include:

- Buying a home

- Car purchase

- Higher education

- Starting a business

Planned savings reduce financial pressure and improve decision-making.

5. Increase Income Streams

Relying on a single income source creates financial risk. Diversifying income improves stability.

Additional income sources may include:

- Freelancing

- Consulting

- Dividend investments

- Rental income

- Online businesses

Multiple income streams accelerate wealth creation.

6. Build Investment Portfolio

Investing is essential for long-term wealth growth.

Common investment options include:

- Stock market investments

- Index funds

- ETFs

- Real estate

- Retirement accounts

Consistent investing helps grow wealth over time through compounding.

Long-Term Financial Goals (7+ Years)

Long-term goals focus on financial independence, retirement planning, and wealth preservation.

7. Retirement Planning

Retirement planning ensures financial stability in later years.

| Retirement Age | Required Planning Period |

|---|---|

| Early Retirement | 20–30 Years |

| Standard Retirement | 30–40 Years |

Starting early reduces the burden of saving later in life.

8. Achieve Financial Independence

Financial independence means having enough income from investments or passive sources to cover living expenses.

Key components include:

- Investment income

- Rental income

- Dividend income

- Business income

This goal represents ultimate financial freedom.

9. Build Wealth Protection Strategy

Protecting wealth is as important as building it.

Strategies include:

- Insurance coverage

- Estate planning

- Tax optimization

- Risk diversification

Wealth protection ensures long-term financial stability.

Net Worth Growth Goal

Net worth is the most accurate measure of financial health.

| Assets | Liabilities |

|---|---|

| Cash savings | Loans |

| Investments | Credit card debt |

| Real estate | Personal liabilities |

| Retirement accounts | Mortgages |

Tracking net worth annually helps measure financial progress effectively.

Income Growth Goals

Increasing income is a critical financial objective.

Methods include:

- Skill development

- Career advancement

- Side businesses

- Passive income creation

Higher income increases savings and investment potential.

Savings Rate Goal

The savings rate determines how quickly wealth is accumulated.

Recommended savings targets:

- Beginner: 10–15%

- Intermediate: 20–30%

- Advanced: 40%+

A higher savings rate accelerates financial independence.

Investment Growth Goal

Investment growth is essential for long-term wealth creation.

Focus areas include:

- Diversified portfolios

- Long-term holdings

- Tax-efficient investments

- Compound growth strategies

Investments should align with risk tolerance and financial goals.

Common Financial Goal Mistakes

| Mistake | Impact |

|---|---|

| No clear goals | Financial confusion |

| Unrealistic targets | Loss of motivation |

| Ignoring savings | Weak financial foundation |

| No investment planning | Slow wealth growth |

| Not tracking progress | Missed improvements |

Building a Financial Goal System

A structured financial system ensures consistent progress.

- Define short, medium, and long-term goals

- Create monthly savings targets

- Automate investments

- Track net worth regularly

- Review goals annually

Consistency is key to financial success.

Final Thoughts

Personal finance goals provide direction, structure, and motivation for building long-term wealth. Without clear goals, financial decisions become reactive instead of strategic. With well-defined objectives, individuals can take control of their money, reduce debt, increase savings, and build sustainable wealth over time.

Whether your goal is financial independence, retirement planning, or simply improving financial stability, setting structured financial goals is the first step toward success. Small, consistent actions today lead to significant financial achievements in the future.